A rebalancing by emerging countries?

According to Jacques de Larosière, in his now famous article published in 2008 the world economy is increasingly financially integrated and capital movements between emerging and “advanced” countries have become massive. What are the medium-term consequences of this integration? To what extent has the world’s financial power not already shifted from the “industrialized” world to that of the emerging countries with a balance of payments surplus?

The following reflections will be organized around three themes: in recent years, the accumulation of spectacular current account surpluses by emerging countries has contributed to a profound change in the distribution of external reserves in the world; the consequences of these changes on global “financial power” must, however, be assessed in a nuanced manner; the international monetary system is far from having adapted to the new global financial situation.

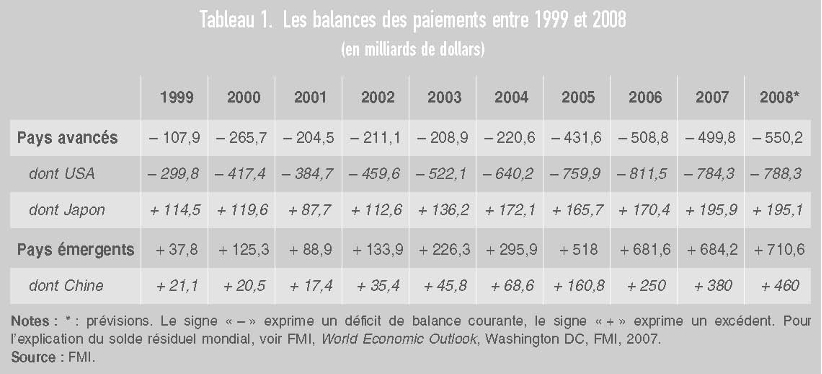

These figures are of considerable economic significance: the US deficit reached 6.2% of its gross domestic product (GDP) in 2006 (5.7% estimated for 2007). As for China’s surplus, it represented 9.4% of its GDP in 2006 (11.7% estimated for 2007). These orders of magnitude represent historical records and reflect, in truth, a paradoxical situation. Traditionally, industrialized countries had balance of payments surpluses and exported their surpluses to developing countries. Today, we are witnessing the opposite phenomenon: it is the so-called “emerging” countries that have become the creditors, if not of the industrialized world as a whole (the European Union is in balance and Japan has a surplus), of the United States, whose current account deficit is entirely offset by capital inflows from emerging countries.

Spectacular surpluses for emerging countries

The extent of the phenomenon

The following table provides a measure of the major changes in the distribution of global balance of payments deficits and surpluses over the past decade.

These figures are of considerable economic significance: the US deficit reached 6.2% of its gross domestic product (GDP) in 2006 (5.7% estimated for 2007). As for China’s surplus, it represented 9.4% of its GDP in 2006 (11.7% estimated for 2007). These orders of magnitude represent historical records and reflect, in truth, a paradoxical situation. Traditionally, industrialized countries had balance of payments surpluses and exported their surpluses to developing countries. Today, we are witnessing the opposite phenomenon: it is the so-called “emerging” countries that have become the creditors, if not of the industrialized world as a whole (the European Union is in balance and Japan has a surplus), of the United States, whose current account deficit is entirely offset by capital inflows from emerging countries.

Emerging countries have three quarters of the world’s reserves

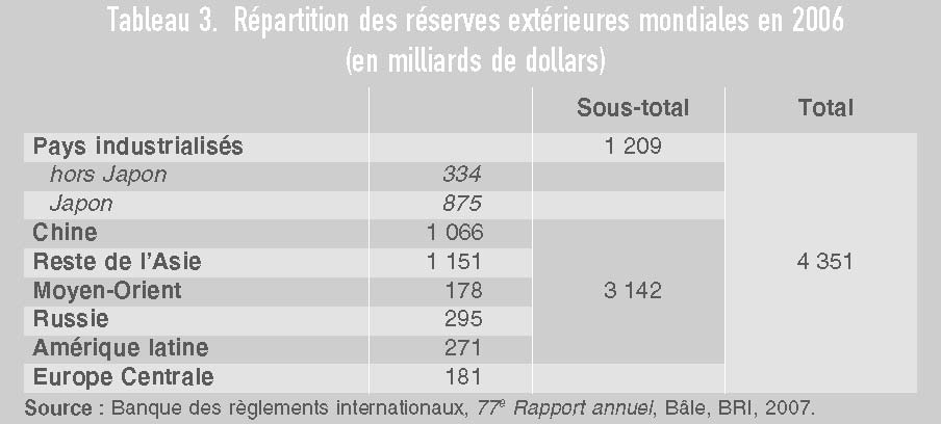

The increases in the external reserves of these countries over the past decade (thanks in large part to successive current account surpluses) are striking.

As a result of these changes, the total amount of reserves held by emerging countries exceeds $3 trillion (compared to less than $1 trillion in 2000) and represents 72% of world reserves (compared to 59% in 2000). Thus, China today holds more than 1.4 trillion dollars with currently a monthly increase of around 40 billion dollars (Bn$). It has thus become the world’s leading investor. This is a profound change in the international financial balance. The United States is now a net debtor against countries like China which enjoy a strong creditor position.

These changes benefit emerging economies in many ways

This mass of reserves at the disposal of emerging countries offers them significant advantages:

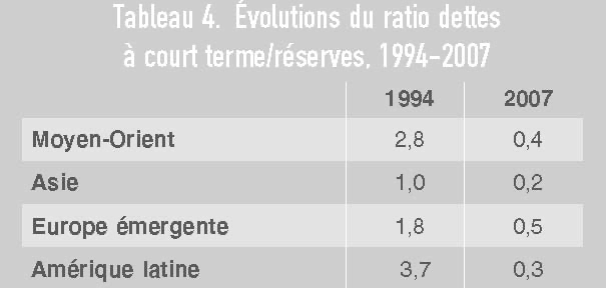

it provides the liquidity and security that Asia lacked during the 1997 financial crisis;

By allowing loan repayments, it loosens the constraint of external debt which, until recent years, limited these countries’ room for manoeuvre (and even subjected them to the “conditionality” of the International Monetary Fund [FMI]).

It helps stabilize the financial markets of these countries, whose exchange rates were previously very sensitive to the volatility of capital movements, a volatility itself exacerbated by the low level of external reserves in many of these countries;

It partly explains – at a time when the economies of the industrialized countries, and in particular the United States, are beginning to slow down – the continued strong growth in the emerging world, a growth that is undoubtedly less dependent today on variations in the economic cycle of the “advanced” countries than was the case seven or eight years ago. The rise of the middle classes and the growth potential of domestic consumption in these countries make their economies less directly dependent on external conditions. However, a prolonged recession in the United States would have a significant impact on emerging countries because of the reduction in imports from the United States;

It gives emerging countries an instrument of power, or even pressure, through the choice of ways to hold their balance of payments surpluses (reserves invested in Treasury bills or acquisitions of various assets on the financial markets of advanced countries).

Despite these advantages, locking up a large portion of their savings in reserves with relatively low returns represents a significant “opportunity cost” for these countries. Investing a significant portion of these surpluses in their own economies that are experiencing high growth rates would, no doubt, be wise [1][1]In addition, sterilizing intervention (currency purchases)… in the long run, and would reduce the amount of current surpluses.

The reasons for this reversal

They can be briefly described as follows:

The United States has followed an expansionary monetary policy for at least a decade, which has resulted in low interest rates and encouraged domestic consumption. Thus, domestic savings (especially household savings) did not finance the country’s investment needs. This shortfall in savings (reflected in the U.S. current account deficit) required the use of external capital. This capital came largely from Japan and especially from the emerging countries, which for their part had a “savings surplus”;

But if emerging countries have been able to accumulate surpluses, it is also because they have significantly improved their own economic management. Indeed, in recent years, many emerging countries have put their public finances in order and strengthened their banking systems while undertaking structural reforms to increase the productivity of their economies. These actions have borne fruit: the chronic indebtedness of some of these countries has been greatly reduced as a result of the budget surpluses recorded. In addition, an increasing orientation of many of these countries toward flexible exchange rates-particularly in Latin America-has helped to avoid the return of the exchange rate crises that had so often interrupted their economic development;

However, a less favorable factor concerns the exchange rates of other countries, especially in Asia (China and Japan in particular). The exchange rates of these countries are, de facto, largely pegged to the dollar (to the yen until last summer, because of Japan’s near-zero interest rates, to the yuan, because of the authorities’ desire to maintain a competitive currency through massive intervention). This under-appreciation of certain emerging currencies has obviously favored the exports (and therefore the trade surpluses) of the countries in question and altered the normal play of the foreign exchange markets.

Finally, the rise in energy prices (favoured in particular by the increase in Chinese demand) has resulted in considerable surpluses in the hydrocarbon producing countries. Even more than in the past, these countries – and in particular the members of the Organization of Petroleum Exporting Countries (OPEC) – have a strong position in international relations in relation to “advanced” countries that are increasingly dependent on them.

The consequences of these changes on global “financial power” are nuanced, and three facts should be highlighted.

The rapid growth of emerging countries is resulting in a significant “catch-up” phenomenon

As we know, emerging countries have been the main beneficiaries of the globalization phenomenon. With the opening of trade borders – and their membership in the World Trade Organization (WTO) – these countries have been able to export more and more goods and services to the world market, thus leveraging the competitive advantage of their low wages. This growth [2][2] On average, the annual GDP growth of emerging countries…, driven by exports, has increased their weight in the world economy. Although the GDP per capita of most emerging countries still lags far behind that of advanced countries, their share of total world GDP [3][3]Calculated in purchasing power parity. Voir FMI, World Economic… rose to 48% in 2007 (United States: 19.7%; European Union: 18%; Japan: 6.3%; China: 15.1%; India: 6.3%; Latin America: 7.6%).

It is estimated that if their current growth rates were to be sustained over a long period of time, China and India would represent in 2050 a global economic unit (26.6%) equal to that of the United States (26.9%) [4][4] See S. Poncet, Perspectives à long terme de l’économie….

The increase in the reserves of emerging countries does not give them total freedom of maneuver

Emerging countries have relatively limited options for investing their reserves. To ensure the liquidity of their external assets, they are forced to resort to the deepest and most secure international markets. These markets – stocks and bonds – are those of the United States, Europe and Japan. This is all the more inevitable as the financial markets of emerging countries are still relatively undeveloped (although they have strengthened considerably in recent years).

23Given the pre-eminence of US financial markets and the role of the dollar as a reserve and transaction currency (65% of the world’s external reserves are held in dollars, compared to 24% in euros, with the share of the latter currency tending to grow gradually), it is hardly surprising that the bulk (around 70%) of the reserves of emerging states are denominated in dollars. It would therefore not be in the interest of emerging market central banks to engage in aggressive reserve diversification policies. The bulk of their dollar holdings (invested primarily in U.S. Treasury securities[5][5]With their 3 trillion in reserves, (of which more than 2 trillion are invested…) is such that any ill-considered action could only precipitate a decline in the US currency and lead to a devaluation of their own assets.

In fact, until 2005, the central banks of emerging countries had relatively little diversification in the composition of their foreign assets. But since then, things have started to change.

A trend towards diversification of their external assets

Given the “opportunity cost” that emerging countries face because of the excessive size of their reserves, their desire to diversify their external assets in order to increase their returns is not surprising. This diversification began with the acquisition of long-term U.S. Treasury bills, as well as bills issued by large corporations. But this trend is also reflected in the intention of some countries – notably China – to devote a greater proportion of their surpluses to capital investments through “sovereign wealth funds”.

The institution of these sovereign funds dates back to the 1960s-1970s with the creation of the “oil funds” (Kuwait Investment Authority, Abu Dhabi Investment Authority, followed by Oman, Brunei, Iran and Russia). In addition to these stabilization funds, Singapore created two funds to more actively manage its balance of payments surpluses (Temasek Holdings in 1974, and the Government of Singapore Investment Corporation [GIC] in 1981). In 2003, China established a fund primarily to recapitalize the domestic banking sector (Central Hujin Investment). After Korea in 2006, China decided in 2007 to create an international fund, the China Investment Corporation (CIC), with an initial capital of about $250 billion taken from the reserves of the Central Bank.

According to available indications, the emerging Asian states as a whole intend to increase their existing funds by $480 billion over the next few years, with assets already approaching $1 trillion [6][6]See McKinsey Global Institute “The New Power Brokers”, op….. These sovereign wealth funds often invest through foreign private equity funds, but now tend to invest directly in companies, and may establish their own funds. They are thus competing with the big Western buy-out funds [7][7]“US buy-out reign under threat”, Financial Times, November 14….

This rise of funds often invested in the stock market or dedicated to direct acquisitions is beginning to raise concerns. Some industrialized countries are concerned about the potential dangers of “active” management of the external assets of emerging states. In particular, they are concerned that foreign governments, through these funds, may take controlling positions in strategic companies. They wonder if the temptation will come for these funds to use their assets for political purposes (access to new technologies, gaining competitive advantages…). They also note that some emerging countries, as they engage in large-scale acquisitions abroad, place restrictions on foreign investment in certain sectors of their own economies. To date, funds of this nature have on the whole been professionally managed and have not led to such deviations. This is particularly the case for the IAG, whose investment choices have always been based on return criteria and have not resulted in takeovers (open or disguised).

Some developed countries, such as the United States, have begun to respond by subjecting “strategic” foreign investments to scrutiny (Germany is also preparing to pass legislation that would require foreign investors to notify the Ministry of Finance of their acquisition plans). In this respect, we recall the defensive reactions to certain attempts by emerging market companies to take control (CNOOC prevented from acquiring UNOCAL, Dubai Ports’ takeover of P&D in the United Kingdom, with the difficulties that this transaction caused in the United States). But there is no doubt that such direct and portfolio investment initiatives by emerging countries will increase in the future.

It seems to me that we must act with caution in this area. The trend toward gradual diversification of emerging market asset portfolios is a normal process and consistent with the open economy principles underlying the international system. On the other hand, imposing too many controls on funds that represent little more than 2% of the world’s financial assets would risk encouraging protectionist forces and restricting the fluidity of capital, which is an important factor of economic growth[8][8] In this respect, it can be noted that the Abu Dhabi Sovereign Wealth Fund…. It would therefore be desirable, in order to avoid the disadvantages of protectionist reactions, to arrive at a “code of good conduct” which would ensure that SWFs adopt greater transparency and follow procedures (as the IAG does) likely to reassure host countries about their intentions and their operating and governance methods. Greater openness to foreign investors on the part of some of the countries controlling these funds would also help.

Emerging countries remain net importers of private capital from industrialized countries

One of the paradoxes of the current situation is that, despite their current account surpluses, emerging countries continue to import massive amounts of foreign capital to ensure their growth. While they also export capital, notably to Africa and Latin America – to secure sources of raw materials – in net terms, emerging countries are major importers of private capital.

If, in 2007, the current account surpluses of the main emerging countries (without the CIS) reached $420 billion [9][9]Figures published by the Institute of International Finance:… (most of which came from Asia), net capital flows to these same countries reached $620 billion[10][10]Institute of International Finance (IIF), Capital Flows to…, which helps explain the sharp increase in their reserves ($756bn).

Of the $620 billion in external capital absorbed by this group of countries in 2007, 265 billion was in the form of direct and portfolio investment and 355 billion in the form of credit. This shows that, despite the rise in their external reserves, emerging countries – whose local financial markets are still relatively limited – are dependent on the “global financial system”, and in particular on the investments of large multinational corporations as well as financial institutions in the “advanced” world.

***

We are thus witnessing a transfer of financial power to the emerging countries, but not a substitution of their financial engineering for that of the advanced countries. We must, however, be aware that this “advantage” will, over the years, be limited with the rise in power of their financial institutions: some Chinese banks are becoming “giants” of world finance[11][11] If the opening of the Industrial and…..

What systemic challenges do these changes pose? Essentially, two can be described.

Massive purchases of financial securities by emerging market central banks have contributed to the fall in interest rates and the explosion in liquidity

A recent study[12][12]F.E. et V.C. Warnock, International Capital Flows and US… showed that acquisitions of financial instruments by emerging countries had a significant downward impact on US interest rate levels. Two thirds of this impact comes from Asian central banks. To the extent that these capital inflows weigh on long rates, this tends to reduce the effectiveness of monetary policy (or increase its expansive nature) in industrialized countries.

This is one of the explanations for the famous “enigma” of Western central banks in recent years: why, despite a tightening of monetary policy, long rates remain stubbornly low. It is also an important factor in the growth of liquidity. It should be remembered that abundant liquidity was the cause of the current financial market crisis. Too much liquidity, and therefore low interest rates, pushed investors and financial institutions to seek higher returns through complex products without sufficiently assessing the nature of the risks involved. We know that it was the underestimation of risks and the euphoria of overly liquid markets that were the fundamental causes of the crisis. In this climate of leverage and ease, the defaults seen in recent months in the U.S. mortgage market subprime loans were the “trigger” for investor mistrust and the contraction of the credit markets.

The influence of the monetary policies of emerging countries in the development of this situation cannot be underestimated. If we observe the evolution of M2 over the last four years[13][13] M2 is the total money in circulation, deposits at…, we see that this monetary aggregate has expanded strongly in advanced countries (5.5% annual growth), but that its growth has been explosive in emerging countries (between 15% and 20% per year).

40 This growth in monetary aggregates and, more significantly, in credit, stems from a large number of factors (including the development of securitization, which has increased the turnover of banks’ balance sheets). But some of these factors are related to the “financial power transfer” analyzed above:

- the pegging of their exchange rates to the dollar – and even more so to a declining dollar – has boosted the competitiveness of many emerging countries’ exports, and thus their trade surpluses;

- this asymmetry in the operation of flexible exchange rates has concentrated the effects of the downward adjustment of the dollar essentially on the countries of the euro zone;

- the difficulty for emerging central banks to sterilize the monetary creation resulting from their purchases of dollars on the foreign exchange market has led to an expansionary “bias” in their monetary policies – to which we can add the effects of the growing “bancarization” observed in these countries.

The paradox of current account surpluses in the emerging world has thus not been a neutral phenomenon. It has had, and continues to have, serious global monetary consequences. The weakness of the dollar, the artificial fixity of certain exchange rates, and the excessive accumulation of foreign reserves all combine to weaken the international monetary system and amplify macroeconomic risks.

The abundance of liquidity that has resulted from this development has so far not led to strong inflationary pressures, thanks in large part to the low cost of emerging exports. But it should be noted that the very high growth rates of these countries, combined with the monetary effects of the undervaluation of their currencies, are beginning to produce tensions and overheating phenomena as well as bubbles [14] [14] the “exuberant” rise of the Shanghai Stock Exchange explains that…. We must take into account the increases in oil prices and, more recently, food prices, which are directly linked to the explosion in demand from emerging countries. The rise in commodity prices, exacerbated by the fall of the dollar, if it were to continue, could well end up being felt on price indices, and thus prompt central banks to tighten their policies, with the inevitable consequences that this would have on the world economy.

The functioning of the international monetary system

Developing countries are taking an increasing share in the global economy and finance. The international monetary system should therefore adapt to this new situation and to the multipolar nature of the world today. In this context, the world needs strong multilateral institutions. No great power can now impose its will on another. New relationships of power are born. This is even more true today if we take into account the financial crisis in the advanced markets which, having spared the emerging markets, has contributed to casting doubt on the West’s financial leadership.

The situation clearly calls for some corrections. Is it normal that some countries continue to intervene massively to maintain the undervaluation of their currency in order to secure competitive advantages while their trade surpluses have literally exploded over the last three years? Is it normal that multilateral surveillance of exchange rates, which is one of the IMF’s statutory and fundamental missions, is carried out so timidly?

One can certainly answer that restoring the authority and credibility of the international monetary system requires an adaptation of the institutions concerned. It is clear in this respect that the distribution of the IMF’s capital among the member states – still largely influenced by the post-war situation – does not reflect the current structure of the world economy. Emerging countries – which, as we have seen, represent nearly 50% of the world’s GDP – hold only 40% of the IMF’s capital. It is therefore necessary to carry out an in-depth reform of the quotas. This will have to be achieved, moreover, largely at the expense of European countries[15][15] Europe holds 30% of voting rights for 20% of ….. As for the G7-G8 global governance body, it seems natural that it be extended, as many observers recommend, to China, India and Brazil.

46 But these institutional changes will not, in themselves, be sufficient. The political will must also be there. Will the United States, China and Japan – the three major sources of global imbalances – agree to play the multilateral game and guide their national decisions according to IMF recommendations? So far, the experience on this point has been disappointing. But as the world becomes more integrated, the stakes more massive, and the ability to harm more widely distributed, isn’t it time to engage in real monetary governance (not to mention the governance of the fight against pollution and global warming, which seems increasingly indispensable), and to accept certain internal policy adjustments to better preserve the global balance? This fundamental question is urgent insofar as the time lost today will be much more expensive to make up for tomorrow.

If the answer to this question is no, it is to be feared that systematic protectionism and reciprocity will once again become the rule of the game, to the detriment of economic growth, environmental quality, international cooperation and global political stability.

Notes

- [1]Moreover, the sterilization of interventions (currency purchases) of these countries by the Central Banks presents a non-negligible potential cost. More generally, the “excess” of Asian central bank reserves over traditional holding standards (four months of import coverage or 100% coverage of external debt with a maturity of less than one year) was calculated. For emerging Asia, this “excess” of reserves would be of the order of $800 billion (i.e. an opportunity cost of $100 billion for 2006, i.e. 1% of GDP). See : McKinsey Global Institute, « The New Power Brokers: How Oil, Asia, Hedge Funds, and Private Equity Are Shaping Global Capital Markets », Washington DC, McKinsey Global Institute, « MGI Report », 2007.

- [2] On average, annual GDP growth in emerging countries since 2003 has been 7.6% (compared with 2.6% for “advanced” countries, i.e. almost three times as much).

- [3] Calculated in purchasing power parity. See FMI, World Economic Outlook, Washington DC, FMI, 2007.

- [4] See S. Poncet, Perspectives à long terme de l’économie mondiale- Horizon 2050, Paris, CEPII, n 2006-16. The global “economic distribution” between the countries of the “North” and the “South” would then be more in line with what it was at the beginning of the 19th century.

- [5] With their 3 trillion in reserves (of which more than 2 trillion are invested in dollars), the central banks of emerging Asia account for one third of the total liabilities of the US Treasury.

- [6] See McKinsey Global Institut « The New Power Brokers », op. cit. [1].

- [7] « US buy-out reign under threat », Financial Times, 14 november 2007.

- [8] In this regard, it is worth noting that the Abu Dhabi Sovereign Wealth Fund will invest $7.5 billion in City Bank, which needs to strengthen its capital base. The intervention of the Emirate will represent 4.9% of the capital of the American bank.

- [9] Figures published by the Institute of International Finance: their definition of emerging markets is limited to about 30 countries, whereas the data in Table 2 covers all emerging countries.

- [10] Institute of International Finance (IIF), Capital Flows to Emerging Markets, Washington, DC, IFF, octobre 2007.

- [11] If the opening of the Industrial and Commercial Bank of China’s capital on the stock market raised $22 billion in 2006, the bank is preparing to acquire 20% of the Standard Bank of South Africa for $5.5 billion. This is an example of China’s financial power and influence in Africa.

- [12] F.E. et V.C. Warnock, International Capital Flows and US Interest Rates, Cambridge (MA), NBER, « NBER Working Paper », n12560, 2006. In the hypothetical case that foreign purchases of U.S. Treasuries fall to zero for one year, U.S. long-term rates would rise by 100 basis points (see NBER, NBER-Digest, Cambridge, MA: NBER, November 2006).

- [13] M2 is all money in circulation, demand deposits and term deposits of up to two years.

- [14] The “exuberant” rise of the Shanghai Stock Exchange explains why five Chinese companies are now among the ten largest capitalizations in the world (the United States has only three).v One example is Shanghai-listed Petro-China, which has a market capitalization of about $1,000 billion (about twice that of Exxon Mobil).

- [15] Europe holds 30% of the voting rights for 20% of the world economy. China has voting rights comparable to those of the Netherlands.

Source : https://www.cairn.info/revue-politique-etrangere-2008-2-page-415.htm